Join Jennifer and Mike in this enlightening discussion as they dismantle five prevalent myths about investing. From the misconception that investing is only for the wealthy to the belief that high risk always leads to high returns, Jennifer and Mike provide valuable insights and practical advice for both beginners and seasoned investors. Learn why it’s never too late to start investing and why savings accounts may not be the safest option for your money. Don’t let these myths hold you back from achieving your financial goals!

MORE HELPFUL LINKS

Summit Video – The Cost of Trying to Time the Market

Check out Our Investment Management

Want to chat more? We’re always here!

VIDEO TRANSCRIPT: Debunking 5 Common Investment Myths

Mike

Alright, so yeah, let’s kick it off. We’ve got a new video for everybody today that we’re excited about, wanting to get back to this as we can and thought of a new topic that we want to talk about. We decided we want to record a video. We’re going to be covering common investment myths today, and it turns out there’s a lot of those. We went through and found several, lots of different investment myths.

We’re not going to cover all of those. We picked out five that we thought pertained to our expertise and as well as ones that we thought were relatively widely known. So that’s what we’ll be talking about today and covering.

So just the format, we’re going to present the myth, talk about why we think it’s a myth today. You know, any kind of myth typically has a little bit of truth to it. So we’ll talk about that element, whatever it is we’re talking about, and then try to do our best to debunk those.

Jennifer

Yeah.

Mike

So, number one. You want to introduce number one for us?

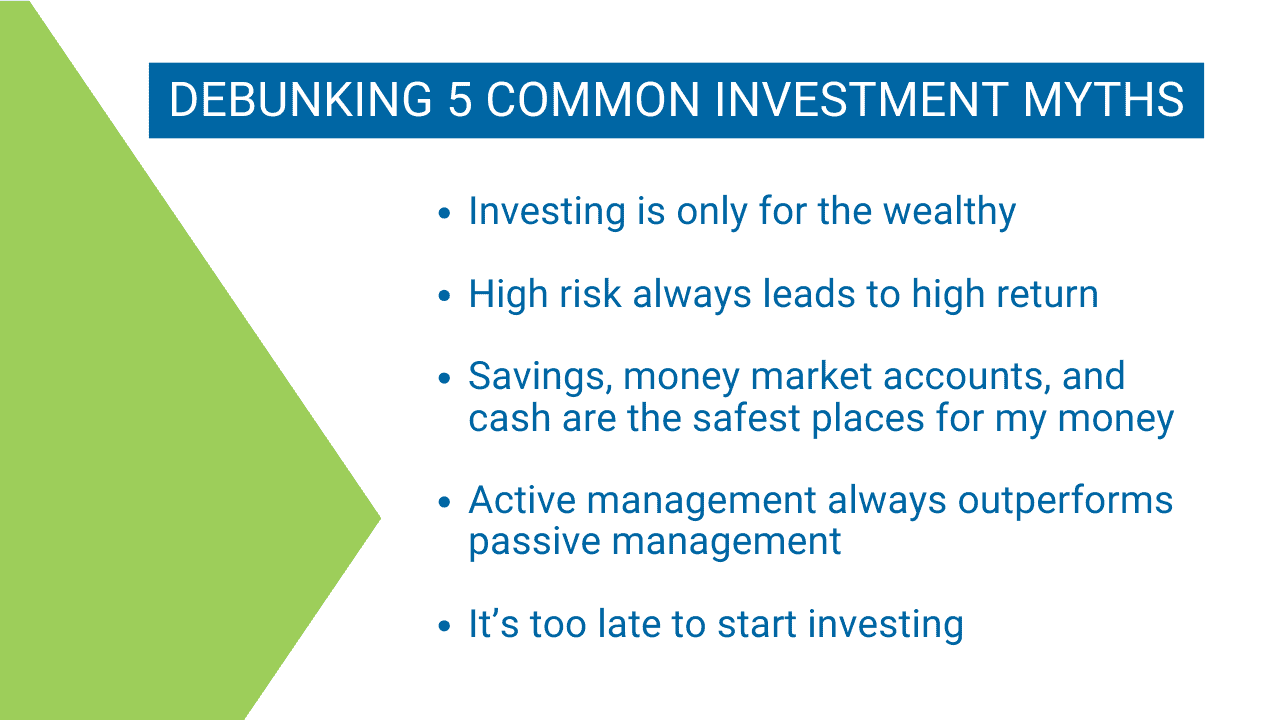

#1 – INVESTING IS ONLY FOR THE WEALTHY

Jennifer

Yes, investing is only for the wealthy. And this is a pretty harmful myth because people tend to believe if they don’t have a lot of money, they can’t really invest. But there’s a lot of power in investing and really just starting with small amounts can be powerful over time.

An example would be for my now 17-year-old daughter. I’ve been putting $100 a month aside for her for not that long, just a few years, and now I’m afraid to tell her there’s several thousand dollars in there. And when she’s 18, you know, technically it’s hers.

So, maybe that wasn’t the wisest. But my point is that it really didn’t take a lot to start really building some wealth for her, for her college years, because it will get consumed quickly. So, yeah, it’s really something. Don’t let that be a self-limiting belief because it’s harmful too. And there’s data that shows a lot of the middle class just don’t invest, and so they lose out on the power of that investing.

Mike

Yeah, and historically there was some truth to that, in that there were more barriers that were kind of there.

Jennifer

Yeah, large transaction costs. And yeah, just for a broker or anybody to talk to you, you needed some wealth. But that’s definitely not true anymore.

Mike

Yeah. The emergence of the common talk today are mutual funds and ETFs, kind of these ways to have a diversified portfolio, and those are relatively — I shouldn’t say relatively new, but they kind of are. They didn’t exist 100 years ago. Where they’re, as far as we look at the decades past.

But yeah, kind of to your point in thinking of your daughter and somebody that is just brand new to it, and you kind of have this thought of it, of investing only being for the wealthy, that “I don’t have the knowledge”, “I don’t have the high enough wealth to cover the fees or the expenses to open up something like this,” “I have no idea even where to start.” It’s actually pretty simple these days.

We did a little bit of research before this, just I was curious myself to look it up. But four of the largest, and I’m going to name them, that I think are probably recognized names, is Fidelity, Vanguard, Schwab, and Robinhood. Those are four common platforms that we hear of all the time. We use some of these, Schwab is one of our main custodians right now. All four of those make it really easy to open up accounts, and they’re really inexpensive. Each one of them have zero minimums, and the fees are really, really low. And not only can you open an account really easily with each of those, it takes very little to know how to actually invest that money.

Jennifer

Yeah, they usually have guides that’ll step you through, what you’re looking for. What we would in general recommend is that, and we’ll talk about this a little bit more later, but buying an ETF or a fund that has lots of investments in them, several thousand stocks usually. Especially if you’re starting out small, start out with a stock market where you get more growth over time.

#2 – HIGH RISK ALWAYS LEADS TO HIGH RETURNS

Mike

Yep. Yep, so that’s number one, that you don’t need to be wealthy to start investing. So, myth number two we’re jumping into is that high risk always leads to high returns.

Jennifer

There’s a grain of truth here, but —

Mike

Yes. There’s definitely an element that to achieve high returns you have to take high risks. And like Jennifer said, there is some truth to that. You need to be willing to take some risks to achieve some higher returns. And there’s lots of examples of that and where that exists. There are no sure things. These get rich quick sort of ideas and schemes, that there’s no risk involved and you’re going to have huge returns from this, that’s not real. There is an element of needing to take some high risks. However, the myth there that all high risks are going to lead to high returns is not necessarily true.

Jennifer

Yeah, I think the general truth behind that is that the stock market offers you the highest returns and it also has the highest volatility. But as long as you own lots of different stocks, that generally holds true. The higher the volatility or risk, the greater the return over time.

However, if you have a more concentrated position and pick stocks, for example, or the example we came up with that we thought was a really good illustration of this is research in motion, which there’s a movie about, I’m dying to see it. I saw like a little tail end of it. They were the maker of the BlackBerry phone and BlackBerry was my first real cell phone. I loved that thing. Anyway, they were cutting edge for sure. And their stock price went to $140.

Mike

2008.

Jennifer

2008. You can see my notes below me, and I cannot. But if you see the movie you can see they were resistant to change. And then the next thing you know Apple just cut their legs off. And by 2011 the price was $7.09?

Mike

$7.09.

Jennifer

$7.09, thank you. Remembered that one. And so that is an example of how — well, it’s an example of a lot of things, right? But that was a lot of risk because if that was the only stock you owned or one of the few, you pretty much lost it all, which really doesn’t happen in a mutual fund, a normal fund with lots of different holdings in it. The other kind of part of it is sometimes our own human brains think if we’re familiar with something, it’s a good investment or a good risk, and that’s not always true. There’s lots of examples of that.

Mike

Yeah. So having a more diversified — in that era you could be, in 2008 we’ll say, having investments in tech and a little bit more broad where you’re still capturing growth of something like a BlackBerry because they were a great company for a period, that you’re taking much less risk, getting to experience some of the growth, and not seeing that full downside of going to zero, right?

Jennifer

Yeah. There is some trade-off there, right? You might not shoot the moon, but you also don’t risk losing it all. And that’s hard. The current story is Nvidia.

Mike

Yeah.

Jennifer

And it’s just been phenomenal what it’s done. And it’s great conversation. Like, “Well, I bought Nvidia, whatever it might be.” I did not buy Nvidia. Mike did. But it makes great conversation. People love to talk about their winners like that. But who knows? There’s lots of competitors. Can’t keep going like it has price-wise.

Mike

Yeah, and timing is always an issue or an element to that as well (See: The Cost of Trying to Time the Market) If you’re constantly taking the highest risk, you’re going to see the most volatility, in most cases. That typically correlates there, coincides.

So, if you needed access to certain funds within a certain period, and it was a short period, you’re looking at a two-year window. I was just talking to my brother about this. I was asking him about, “Hey, I need to save some money” for a project he’s working on and wanted to know the best vehicle for that, but he needs the money in two years is his window that he’s looking at. For that purpose, I definitely wouldn’t recommend any kind of high-risk portfolio, even a well-diversified one, right?

Jennifer

Yeah, right.

Mike

And now we’re looking at a time horizon to say that, yeah, over a decades-plus long period, diversified higher risk is typically going to show you a higher return. But going back to debunking that myth there, it doesn’t always hold to fruition because there’s a very real possibility that two years from now, that investment is going to be worth less than it is today. And in that case, it did not lead to high returns.

Yeah, so that was myth number two.

Jennifer

I’ll pull up the paper notes. I’m sorry.

Mike

Since our computer just went to sleep on me.

#3 – SAVINGS, MONEY MARKET ACCOUNTS, AND CASH ARE THE SAFEST PLACE FOR MY MONEY

Jennifer

Yes. Myth number three. Savings, money market accounts, and cash are the safest place for my money. So, this is always a really interesting one because our human brains really like the thought of, “I put a dollar in, I make some interest…” (Now you make a little interest. Recent years, not so much.) “And then I get a dollar out. I am good.” And it’s more tempting now because rates are a bit higher, 4% in some savings, maybe a little bit more. But for quite a few years, it was zero that you were making in money market funds. And so, that feels safe. However, in recent years, inflation has also been totally out of control.

Mike

Yeah.

Jennifer

It’s moderated now. Prices haven’t really gone down. Some have a little, but inflation has stopped growing as fast. That’s like the lingo, the game with the language around this is, “Well, inflation’s down.” Well, that means the growth rate of inflation is down, not that everything’s gone back to pre-2020 prices.

Mike

Yeah.

Jennifer

So, if what you’re buying is inflating at a faster rate than any kind of interest rate you can make on a safe investment, you’re losing money because the buying power of your money is reduced. And you can see this in this chart. And this chart is money market, I mean, treasury bill returns since 1926.

And every time you see red, that means inflation was higher than the yield of that, of the treasury bill at that given year. These are all years, just as a way. So, it’s not true every year, but it definitely is true often.

Mike

Yeah. And that’s the assumption that you’re actually putting the money in treasury bills.

Jennifer

Well, that’s true.

Mike

There’s the, I’ll say, even scarier or more at-risk thought of cash, of keeping accounts in checking accounts or even in physical cash.

Jennifer

Yeah, and you get zero return.

Mike

Yeah, and there’s nothing there. And understandably, the thought is, I want to preserve my principles. I don’t want this to be at-risk in the market. This is very important. I need to keep this money. It’s set for a certain thing, you know, whatever it is.

But I’ve given the story before that made it very real to me. You know, I’m in this industry, but fell, I guess, I don’t know, victim to inflation. And we’ll call it that. I’m going to victimize myself here. But I previously, before working with Summit, I had a job that had me doing a lot of travel. And the company I was working with was gracious enough to allow me to accumulate my own miles, right?

And lots of people that do a lot of travel, oftentimes for work, will get some great benefits out of SkyMiles and kind of accumulating those. And at the time, I remember looking at the different airlines. And in Richmond, one of the most common airlines is Delta. But there was the added benefit in my mind that I’m thinking, and Delta has the added benefit that the miles don’t ever expire. They don’t go away.

I can keep them as long as I want to keep them. So, I accumulated quite a bit of miles. And I remember getting to the end of, close to the end of my career with this company and seeing all the miles and just quickly pulling up and looking and seeing, I could fly me and my wife to Europe and back off of these SkyMiles, or really close. We looked at Alaska. I could get to Alaska and back. And in my mind, I thought, I’m going to save these miles, and one day we’re going to take this trip. And it’s going to be a great trip. We had young kids at the time, but I’m going to save these miles. And I look not too long ago thinking, I still have those miles because they didn’t expire, but I also have not continued accumulating and I didn’t use them. So, they just sat there. And the inflation was real for that, just the same. And that those SkyMiles are worth less now, and I could barely get to the Midwest with those same SkyMiles.

Jennifer

Not quite as glamorous as Europe.

Mike

Not quite as glamorous as Europe and getting over there. Yeah. So, that’s the element that there’s a risk factor with buying power and inflation that people don’t realize and don’t think about. Yeah.

Jennifer

Yeah, yeah.

Mike

Yeah. All right.

#4 – ACTIVE MANAGEMENT ALWAYS OUTPERFORMS PASSIVE MANAGEMENT

Mike

So myth number four, active management always outperforms passive management. So, let’s define first, active versus passive. This is something we talk about often, We’ve talked about in past videos, and we talk about with prospects and clients all the time that you can almost view this as a spectrum, right? That the passive side is buying one stock or one mutual fund or one investment. You’re putting the money in one place, and you leave it, you set it, you never, ever touch it for 40 years. It stays right where it is. The other end of the spectrum is, I even hesitate to put day trading in here, but that’d be the extreme, extreme side of the active side of day trading. Going in and lots of turnover. You’re going to outsmart the market, buy the right things at the right time. You’re doing lots of timing and all of the elements like politics (See: Presidential Elections and the Market) and COVID and all these things.

Jennifer

Wars. Lots of stuff.

Mike

I think that this company’s going to outperform. That’s the spectrum. Oftentimes people have this thought or this belief that active management is always going to outperform passive. Some will find this almost paralyzing, that I don’t have the knowledge or the abilities to actively manage so I can’t invest at all or I’m not going to be able to make as much.

Jennifer

Yep, it applies to mutual funds too. Passive is index funds. I’m going to buy just whatever S&P 500, whatever they say. I’m going to own those 500 stocks. And an actively managed fund might say, they don’t do day trading for the most part, but they do a lot of, I think British Petroleum’s going to outperform Exxon so I’m going to buy British Petroleum and sell Exxon. It’s just all of that trading.

What we see over time is that’s far from true because none of us have a crystal ball and we just don’t know. The data shows, though, that sometimes that’s true, in some years, but it’s not generally true at all. Part of it too is transaction costs. You’ve got taxes and sometimes commissions, depending on where you’re doing all this trading, and depending on the mutual fund too. The mutual funds, when there’s a lot of churn, there’s a lot of taxation that happens and a lot of transaction costs as well. We’re not a true just buy the index and sit with it, but we prefer that to the super active where people are trying to predict what’s going to happen next. Because of this, over time, you have a higher probability of success if you’re not trying to predict what’s going to happen.

Mike

Yeah, and you’ve got the added cost to that as well. When somebody’s actively trading and actively managing, as far as hiring somebody and going and looking for an active manager versus a passive manager, that the active manager, I’d say rightfully so, is going to be charging you more money.

Jennifer

It’s a lot more expensive.

Mike

Because they’re doing a lot more work. A lot more work that we feel that is maybe spinning their wheels, potentially a little bit, because it’s really difficult to consistently beat the market with those kind of choices.

Jennifer

Nobody can. Nobody has.

Mike

So yeah, that’s number four. Number five, our last one.

#5 – IT’S TOO LATE TO START INVESTING

Jennifer

It’s too late to start investing. Yeah, that’s really kind of self-defeating thinking in that — you know, I understand it, right? You’ve got to worry about market risks because markets are volatile in the short run, but I’ve definitely seen it where clients have started saving later in life. And really, anything you can do to pad your future years, anything is better than nothing. Even if it’s small.

Going back to my daughter’s $100 a month, it does, it will make a difference for her as well. She’s young, but she’s going to need the money soon for college. So, you really need to create a safety net for yourself, even if it’s not a large one. That I think a small, you know, if it’s small and late, if you’re investing for 10 years versus 40, you won’t be as wealthy, but you will have a safety net of some sort.

Mike

Yeah, yeah, the idea of compound interest is far from a new one. It’s not really a myth. People know and understand that.

If you do any kind of research, it’s really easy to see that. But when people fall into this trap of the thought of, “Well, compounding interest is true, and because I didn’t start decades ago, it’s too late for me now.”

So, just to flip that on its head and to kind of present that as this fallacy and this myth. I’ve taught some adolescents or kids different investment and financial topics, and one of the ones we talk about is compounding interest. I use this illustration.

It’s a really cool illustration that shows two different kids side by side. And I’ll usually use one as an example and I’ll have them stand up and I’ll say, “Okay, so now imagine that at age 19…” They’re both 19 years old, both of them. They get their first job, and they start investing $2,000 or they have enough to save $2,000 a year, okay?

But one of them decides, I’m going to start right now with my new job and I’m going to save $2,000 a year, and he does it for eight years and then he stops, okay? And the other one.

Jennifer

This is powerful.

Mike

Yeah, the other one waits. He does not start at age 19.

Instead, he spends his money for the first eight years. And you guys are welcome to take this and share this with your kids because of the power of this. Instead, he waits eight years and then starts to save $2,000 a year at age 27.

And they both continue this journey. The first one, remember, only for the first eight years. The other one didn’t start until age 27 and then he started saving $2,000.

But the second one saves $2,000 every year all the way until age 65. So, for the rest of his life, he saves $2,000. So, I don’t even know how many years that is.

It’s almost 40 years that the second one is saving $2,000 a year. The first one, by starting eight years earlier, comes out so much further ahead. And the interest rate we’re using is a high one and I realize maybe not sustainable. But for illustration purposes, we’re using a 12% return on this money.

Jennifer

Nice one. 100% equity.

Mike

Yeah, so it’s a 100% equity.

And at 19, people potentially have the flexibility to do that. So, to put this money away. So, the difference in the wealth is almost a million dollars. It’s like $700,000 in difference for the one that saved much less. Like the money that went into it was much smaller but just started earlier. Now, here’s the fallacy or the thought.

The people will hear that and they will think, “Well, I’m not 19 anymore and I can’t do this anymore.”

Jennifer

Right.

Mike

If that was true at age 19, that doesn’t go away today. Compounding interest is still true today. It’s true that you can’t go back to 19. But you’re still today and a decade from now, you still could have started 10 years earlier.

Jennifer

Yeah.

Mike

So, there’s always now, you can always start today. One thing that we talk about often with clients that come in is they are in their 50s or 60s and they start to think about the conversation is usually around becoming much more risk averse and taking their money out of because they’re approaching retirement. And they thought that, I’m about to start spending money and all the media says that I should be coming out of the stock market.

But one of the things that we present often is at age 60, you potentially have another 30 plus years of living. That’s still a long time.

Jennifer

It is.

Mike

A long time for compounding interest to work in your favor.

Jennifer

Yeah. Yeah. And kind of tying that. I remember when I was thinking about going to grad school, I was like, I don’t want to go every night. I mean, I went usually three nights a week and then did homework all weekend. I was like, do I really want to do that? And then I started thinking, well, the time is going to go by anyway, so how do I maximize my use of that time? Right? And so that’s how I talked myself into it. But it’s true for this too. The time is going to go by anyway, so you might as well capture what you can of returns while you can. And sometimes that’s not just for you, but for your heirs, that it will continue to grow for them if you don’t spend it all later.

Mike

I did the same. I went and counted the same illustrations, that same $2,000. If you started that by age, what was it? 57. Right? So, you retire by 65, you’re 57 years old and you start doing that $2,000.

Even though you’re within 10 years, you’re only going to be able to save for another eight years. But you save for those eight years, $2,000 a year, and it would have to be 100% equities. But we put this away and you’re saving an aggressive —

Jennifer

As long as you do that intentionally.

Mike

Yeah. By 90s. And let’s maybe consider this as something that is, you’re just setting this aside for heirs, that you’ve got money for yourself. But by age 90, by 91, you’ll have over $400,000.

Jennifer

Wow.

Mike

In a $2,000 a year. So that’s now your late 50s that you start doing the $2,000 a month.

Jennifer

It’s real money.

Mike

It’s real. So compounding interest was true when you were in your teens and 20s. It’s true today just as well. Whatever age you’re at, starting now, it’s never too late to start.

Jennifer

Yeah, for sure. And you know, everyone’s experience will be a little different. 12% is probably not as sustainable. But long-term returns are 9%, 10% in equity markets. And so, I think the 12% is potentially achievable too because you’re dripping money into different markets. But yeah, the math is still the same, or true either way once you compound your returns over time.

So yeah, I don’t know if that dispelled any myths for you, but it was kind of fun to research.

Mike

Yeah, it’s fun to look at it. I think one thing that we maybe take for granted in just being in this industry, there’s lots of myths that we hold in other industries that we just don’t know because we don’t know. So, hopefully that’s something that you’re hearing, and it’s maybe changing your thinking about that a little bit.

And we would always encourage you to talk to a financial professional. There are less barriers to being able to do that than you realize. You’re welcome to give us a call, but it doesn’t need to be us.

Give anybody a call. And yeah, I think that’s it for today.

Jennifer

Okay, thank you.

Mike

Until next time. Thanks.